APR, which stands for Annual Percentage Rate. APR is the yearly rate that is charged on borrowing or earned on an investment. The rate is expressed in terms of a percentage and represents the actual cost of funds on an annual basis over the term of a loan.

APR takes into account any additional costs or fees that are incidental to the transaction but excludes the compounding from the equation. As mortgage loans and credit arrangements (for e.g. credit cards) tend to vary considerably in terms of interest-rate structures, late penalties, transaction fee, and other variables, a standard calculation like the APR gives borrowers a bottom-line number which they can easily compare to rates offered by other lenders.

Laws mandate that mortgage loan issuers and credit card companies must disclose to their customers the APR they charge for facilitating a clear and easy understanding of the actual rates that apply to their agreements. Credit card companies have been permitted to advertise their monthly interest rates, but they are also under an obligation to clearly disclose the APR to borrowers before signing the agreement. As an example, a credit card may charge 1% on a monthly basis, and its APR will be 12%.

Loans have either variable or fixed APRs attached to them. A loan with a fixed APR has an interest rate which will not fluctuate or change during the term of the loan or credit facility. In contrast, a loan with a variable APR has an interest rate that can fluctuate at any time.

What’s The Difference Between Interest Rate Vs APR

A nominal interest rate, commonly known as the interest rate, is used to refer to the interest rate which is charged on a loan, and it does not take into consideration any other costs that are incidental to the loan transaction. On the other hand, APR aggregates the nominal interest rate and other expenses or fees associated with the procurement of the loan. This is why an APR is usually higher than the nominal interest rate of the loan.

As an example, if you are availing a mortgage worth $ 200,000 that has a 6% interest rate, your yearly interest expenses would be $ 12,000, which is equivalent to a monthly payment of $ 1,000. But let us assume that your home purchase entails mortgage insurance, closing costs, and loan origination fees that are worth $ 5,000. For the purpose of determining your APR on the mortgage loan, these additional expenses are added to the original amount of the loan to come up with a new loan amount of $ 205,000. This interest rate of 6 % is then used in calculating a new yearly expense of $ 12,300. Dividing this yearly payment of $ 12,300 by the original amount of the loan which is $ 200,000 yields an APR of 6.15 %.

According to the Truth in Lending Act, lending companies are required to state the APR along with the nominal interest rate in every consumer loan agreement. The scenario which confuses most borrowers is when 2 lenders offer the same nominal rate but different APRs. In this situation, the lender offering the lower APR requires fewer upfront costs and offers the better deal.

RELATED: 6 Secrets to Save Money at Amazon

Annual Percentage Yield (APY) vs. APR

An APR only considers simple interest. On the other hand, annual percentage yield (APY), which is also called effective annual rate (EAR), takes into account compound interest which is applicable to the loan. Therefore, an APY is generally higher compared to the APR on a loan of the same amount. When the rate of interest increases, and the compounding periods get smaller, the difference between APY rate and APR rate magnifies.

Consider a loan with an APR of 12 %, which compounds on a monthly basis. If a borrower has taken out a loan of $ 10,000, his monthly interest will be 1 percent of his outstanding balance or $ 100. This will have the effect of increasing his outstanding balance to a slightly higher $ 10,100. The next month, this interest rate of 1% is charged on this higher balance, and his interest expense will be $101, which is slightly higher compared to the prior month. In case this balanced is carried for one complete year, the effective interest rate will be 12.68 percent. APY takes account of these small changes in interest expense due to the effect of compounding, while APR ignores it.

Let us take another example to make a comparison of an investment that yields 5 % on an annual basis, with another that yields 5 percent monthly. For the former, the APY and APR are both equal to 5%. But in case of the later, the APY is 5.12 percent, which reflects the effect of monthly compounding.

Because an APY and a different APR can be used by companies to express the same rate of interest, it is generally the case that both borrowers and lenders will stress the more favorable number to present their position (the Truth in Savings Act of 1991 mandates that both APY and APR be stated in, contracts, ads and agreements). Banks and financial institutions will usually advertise the APY of a savings account in a larger font and the relevant APR in a smaller font size, because the APY represents a superficially large number. However, when the bank is a lender usually the opposite happens, as it tries to persuade its customers that it is offering a lower rate.

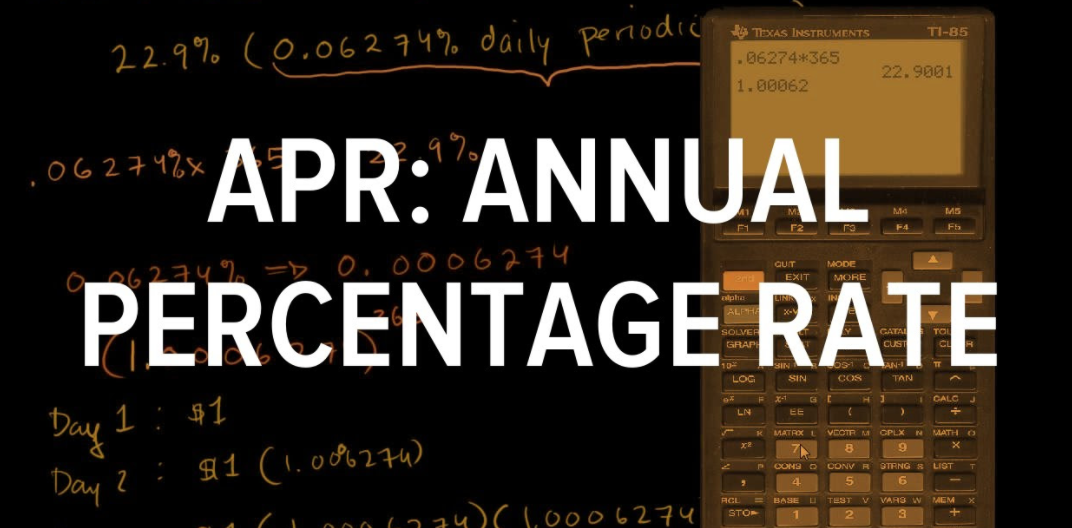

Daily Periodic Rate Vs APR

The daily periodic rate is the rate of interest which is assessed on the balance of a loan on a daily basis. It is effectively a loan’s APR divided by 365, representing the number of days in one year. Likewise, the monthly periodic interest rate is a loan’s APR divided by 12. Both credit card providers and mortgage lenders are permitted to disclose their monthly APR provided that the full 12-month APR is disclosed somewhere before signing of the agreement.

Can APR be Misleading?

Plenty of above examples illustrate that APR can mislead relevant parties about the actual costs associated with a mortgage or credit card loan. Some experts contend that the APR is best when comparing long-term loans in terms of their costs. Even in case of a short-term debt, like a seven-year note, the APR tends to understate the expenses associated with the loan. This usually happens because APR calculations work on the basis of long-term repayment schedules; for mortgage or credit card loans that have shorter repayment periods or are repaid quickly, these expenses and fees are spread too thin with APR calculations. The average yearly effect of closing costs tends to be much smaller when these costs are spread over a 30 year period instead of 7 or 8 years.

APR also has the tendency of running into similar troubles when it comes to adjustable-rate mortgages. APR calculations always assume a fixed rate of interest, and although APR calculations always take rate caps into account, the final figure we are presented with is still calculated on the basis of fixed rates. As the interest rate charged on an adjustable-rate mortgage tends to be uncertain once the fixed-rate period lapses, APR estimates can immensely downplay the actual costs of borrowing if mortgage loan rates rise in the near future.

How Credit Card Companies Determine APR?

Most credit cards tend to carry floating APRs, which is commonly referred to as variable APRs. These credit cards feature floating interest rates that fluctuate depending on the market variables or the U.S. prime rate or an index. The companies set APRs by incorporating this variable element and adding their profit margin to it. For instance, if a credit card company charges a 10% profit margin and the prime rate is 5 %, the borrower will have to pay a 15% interest rate.

Although they are rare, a few credit cards feature a fixed interest rate. In case of credit cards (unlike other kinds of loans), a fixed APR means the interest rate will not change, until the lender decides to do so. However, a prior notice in writing is required to change it, and this adjustment is only applicable going forward, and not retroactively.

In a few situations, credit card companies provide different APRs for different kinds of charges. For instance, a credit card may offer one APR for purchases, a different one for cash advances, and third one for balance transfers from another credit card. Likewise, banks tend to charge high-rate APRs penalizing customers who are late on their payments or have breached other terms and conditions of the cardholder agreement, while offering low-rate introductory APRs to poach new customers – ideally those who carry a balance on their cards.

Introductory or low APRs can beneficial for personal finance if the borrower manages to use them carefully. An outstanding balance of $2,000 on a loan which has a 12% APR incurs $20 in interest charge each month. However, transferring this amount to a credit card, which has an introductory APR of 0% for 12 months, enables you to apply the saved $20 to reduce the principal, paying off the balance much sooner.

Understanding APR is crucial for making informed financial decisions, whether you’re borrowing or investing. While APR provides a standardized way to compare loan costs by including fees and additional charges, it’s not without its limitations. For shorter-term loans or those with variable rates, the APR might not fully represent the total cost. Therefore, consumers should also consider the impact of compounding interest (APY), the term of the loan, and potential changes in interest rates for adjustable loans. By doing so, you can better navigate the complexities of borrowing and ensure that financial products align with your long-term financial health. Remember, the lowest APR isn’t always the best deal if other terms and conditions don’t suit your financial strategy. Always read the fine print and possibly consult with a financial advisor to fully grasp the implications of any financial agreement.